Executive Snapshot

Initial Investment Thesis

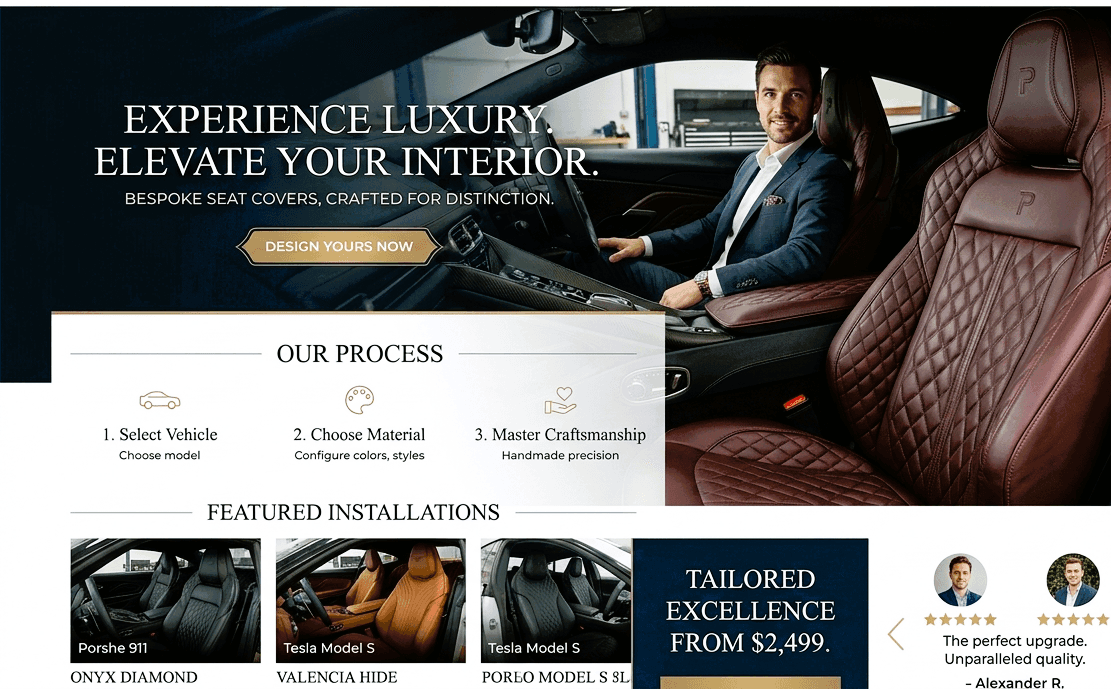

A differentiated, high-AOV ($430–$500) custom automotive brand with defensible operational advantages (VIN-based precision ordering, complex-seat capability, and phone sales infrastructure driving 35–40% of revenue). Strong paid media engine already built, team in place, and clear levers for scale (SEO, content expansion, material diversification, CVR optimization).

Initial Concern Flags

Heavy reliance on paid traffic (Meta + Google only), low conversion rate (0.6–0.7%), and fully made-to-order custom production from China create operational and margin risk. Business also depends meaningfully on phone-based abandoned cart recovery and specific supplier relationships.

Market & Demand Signals

Category Overview

Custom automotive seat covers sit within the broader automotive aftermarket industry, which historically performs well due to long vehicle lifespans and owner personalization trends. This brand focuses on high-ticket, custom-fit leather covers — a premium niche within a large, fragmented market dominated by universal-fit, lower-quality options.

Market Size & Growth Trajectory

The U.S. automotive aftermarket exceeds $400B annually, with interior accessories representing a stable sub-segment. Growth is driven by:

Increasing vehicle age (avg. vehicle age in U.S. continues rising)

High truck ownership rates

Strong used vehicle market

DIY and personalization culture

Premium customization is a smaller segment but structurally growing as consumers demand better fit and quality.

Search Demand & Keyword Indicators

Core keywords such as “custom seat covers,” “Ford F150 seat covers,” and “leather truck seat covers” are historically high-volume, evergreen searches. Demand is model-specific and SKU-driven (vehicle-based long-tail keywords), which supports scalable paid + SEO strategies. No indication this is a short-term viral trend category.

Seasonality vs Evergreen

Largely evergreen demand. Mild Q4 lift possible (holiday spending, gifting), but no extreme seasonal dependency. Vehicle ownership needs are constant.

Problem Urgency

Moderate urgency. Seat covers are not essential, but protective and restorative use cases (protecting new trucks, restoring older interiors, resale value) create rational purchase drivers. For truck owners and classic car enthusiasts, fit precision significantly increases perceived necessity.

Cultural/Macro Tailwinds

Rising vehicle prices → consumers maintain vehicles longer

Growth in truck/SUV ownership

Resale value preservation mindset

Increasing consumer skepticism toward generic “custom” claims (VIN-based differentiation is timely)

Regulatory Impact

Minimal regulatory risk. Standard consumer goods category.

Trend vs Timeless

Timeless category with consistent demand, not trend-driven.

→ Market Attractiveness Score: Strong

→ Demand Durability Assessment: High (Evergreen, model-driven, replacement + protection use cases)

Product–Market Fit Indicators

Goal: Does this solve a clear problem for a defined audience?

Value Proposition Clarity

Yes — the value proposition is clear and concise:

“Truly custom-fit leather seat covers (using VIN verification) that fully wrap and fit complex or hard-to-fit vehicle seats.”

The problem being solved is explicit: generic “custom” seat covers often do not fit properly. This brand addresses mistrust in the category by using VIN-level validation and accommodating complex seat types (integrated seatbelts, molded headrests, jump seats, vintage models).

Core Customer Persona

Primary segments include:

Truck owners (e.g., Ford F-150, heavy-duty pickups)

Classic/vintage vehicle owners

Owners of vehicles with complex seat configurations

Buyers seeking interior restoration or protection

High-intent shoppers comparing custom seat cover brands

Demographically: predominantly male, vehicle-proud, value durability and aesthetics, willing to spend $400–$600 for quality and precision.

Differentiation

Operational differentiation:

VIN-based validation (reduces fit errors)

Ability to produce covers for complex seat types

Capability for vintage and specialty vehicles

Phone-based abandoned checkout closing (35–40% revenue impact)

Product differentiation:

Full 360° wrap option

Compatibility with seat functions (cupholders, folding mechanisms)

There is no formal IP protection mentioned, so differentiation is execution-based rather than legally defensible. However, supplier relationships and systems create operational moats.

Commoditisation Risk

Moderate. Seat covers, as a category, are highly commoditized. However, the premium, high-complexity custom niche is less saturated and harder to execute operationally. Risk increases if competitors adopt VIN validation and similar fulfillment systems.

Ease of Customer Adoption

Moderate friction due to:

VIN submission

Potential measurement/photo requirements

High ticket price

Trust concerns around fit

However, phone support and guided assistance mitigate this friction. Low refund rate (0%) suggests high satisfaction or strong expectation setting.

Repeat Usage Potential

Low to moderate. This is primarily a one-time purchase per vehicle. Repeat purchases would depend on:

Multiple vehicle ownership

Upgrading to full custom

Material expansion (e.g., cloth variants)

No natural subscription/refill logic exists.

Price Positioning

Premium positioning.

AOV: $430–$500

COGS: ~$160

26% net margin

Justification for premium pricing includes full custom fit, leather material, VIN precision, and ability to fit complex seat structures competitors avoid.

Website & Conversion Infrastructure

Website Speed & UX Quality

Without direct speed audit data, the site appears built on Shopify with a relatively simple structure — generally supportive of stable performance. However, visible layout issues on the reviews page (which lacks actual content) suggest room for refinement. Key pages load product details, vehicle selectors, and ordering steps cleanly, but conversion-focused elements could be more intuitive.

UX strengths:

Clear vehicle selector for custom orders

VIN / configuration-driven flow supports personalization

Multiple product options presented logically

Warranty and fit info emphasized in product pages

UX weaknesses:

Lack of visible review content on main site

Pages like “Customer Reviews” show static placeholder text without reviews

Mobile Optimization

Likely good (Shopify standard), but no real mobile audit available. Given heavy paid ad traffic, mobile UX must be prioritized; any lag or confusion here could depress conversion.

Visual Credibility & Brand Consistency

The visual style is fairly consistent: professional photography of seat covers, detailed product text, and warranty/fit guarantees. However, brand visuals are relatively generic with limited unique identity cues beyond product shots — this represents a mild credibility gap versus higher-end automotive accessory brands.

SKU Count & Catalog Structure

The catalog covers:

Standard custom seat covers

Full custom seat covers

Floor mats and interior packages

Each SKU uses vehicle and configuration selectors. The structure supports personalization but isn’t overly broad — appropriate for a custom product niche. Bundles (front + back seats) are supported with savings indicated, helping average order size.

AOV (Average Order Value)

Reported around $430–$500, which is solid for a premium seat cover product.

Estimated Conversion Rate

Stated industry data from the business suggests a conversion range ~0.6–1%, which is low but still profitable given the high AOV.

Upsell / Cross-Sell Structure

Some bundling logic exists (e.g., seat cover set discounts), but upsell tactics like complementary products (floor mats, interior makeover) could be more prominent and integrated at checkout and product pages. Opportunities here are unleveraged.

Trust Signals (Reviews, Certifications, UGC)

Weakest area.

Trustpilot shows zero reviews (a 0 score by default) — no social proof from that channel. (Trustpilot)

No visible third-party certifications or badges.

On-site reviews appear generic or potentially self-curated rather than verified (images and quotes).

Public social profiles exist but with limited follower count and content activity (Instagram ~1.7K followers with ~50–60 posts) suggesting modest engagement.

This is a significant gap especially in a high-ticket category where trust can make or break conversions.

Technical Issues Visible Publicly

“Customer Reviews” page exists but has no actual reviews displayed.

Occasional loading issues or unclear imagery reduction on some pages.

VIN and configuration inputs must work flawlessly — any UX bugs here would kill completion but are not publicly visible.

Checkout Flow Friction

Custom orders involve multiple steps (select year, make, model, seat type, colors) — necessary but potentially friction-inducing. The presence of phone support and abandoned checkout calls mitigates some friction, but the checkout timeline (VIN input, measurements, photos for complex orders) creates conversion resistance not fully addressed by UX incentives.

Traffic & Distribution Footprint

Goal: Where does demand actually come from?

Estimated Traffic Volume

Based on Shopify data provided:

1,100 orders

~$549,924 in revenue

AOV ~$500

Conversion rate stated between 0.6%–1%

Using a blended estimated CVR of ~0.7%, this implies approximate annual traffic of:

1,100 orders ÷ 0.007 ≈ 157,000–180,000 sessions annually

(~13,000–15,000 monthly visitors)

This suggests moderate but highly monetized traffic due to high AOV.

Primary Channels

Paid acquisition is the dominant driver.

All sales are generated from:

Facebook (Meta Ads)

Google Ads

There is currently:

No meaningful SEO contribution

No marketplace presence

No organic engine highlighted

No Amazon / Etsy channel

No wholesale or B2B distribution

The business is therefore 100% paid-media driven.

Channel Concentration Risk

Very high concentration risk.

Two ad platforms drive essentially all revenue:

Meta (Facebook)

Google

Additionally:

35–40% of monthly revenue comes from abandoned checkout phone calls.

This creates a dual dependency:

Paid ad lead flow

Phone sales team converting abandoned carts

If paid traffic slows, the phone sales pipeline shrinks proportionally.

There is no evidence of:

Email-driven repeat revenue

Organic search pipeline

Influencer engine

Affiliate program

Retail presence

This makes revenue acquisition fragile but controllable (through ad spend).

Platform Dependency Risk

Meta + Google dependency is high.

Risks include:

CPM inflation

Account bans or restrictions

Policy changes

Ad creative fatigue

Increasing CAC

However, the business benefits from:

High AOV ($430–$500)

26% margin

Backend phone closing (7% close rate)

This provides more cushion than lower-ticket e-commerce models.

The ad agency charges a percentage of sales, which aligns incentives but creates cost variability tied to performance.

No TikTok, Pinterest, or YouTube diversification is mentioned.

International vs Local Reach

The primary market appears to be the United States.

The business is based in Florida.

Shipping is handled from China with 7-day shipping times (implies U.S.-focused fulfillment routes).

No indication of strong international expansion yet.

Potential exists to expand into Canada, Australia, UK (truck markets), but currently appears U.S.-centric.

SEO Footprint Strength

Explicitly stated:

“SEO hasn't been utilized at all yet.”

This is a major gap.

Given:

Vehicle-specific long-tail keywords (e.g., model + seat covers)

High-intent search behavior

Poor reviews from competitors (opportunity for comparison content)

SEO represents a strong unrealized acquisition lever.

At present, organic presence should be considered weak to minimal.

Marketplace Presence

No Amazon, eBay, Etsy, or other marketplace footprint mentioned.

This keeps brand positioning premium and controlled but limits distribution diversification.

Entering Amazon would:

Increase exposure

Compress margins

Reduce brand control

Increase commoditization pressure

Currently, the brand remains fully DTC.

Direct vs Intermediary Sales Ratio

Appears to be 100% direct-to-consumer via the owned Shopify store.

No wholesale

No dealer network

No marketplaces

No retail presence

Phone sales operate within the DTC funnel (not external distribution).

Structural Observations

Strengths:

High AOV supports aggressive paid acquisition

Strong backend monetization (phone closer system)

Dedicated creative + editing team

Established ad systems

Hands-off fulfillment process

Abandoned checkout recovery significantly increases LTV per lead

Weaknesses:

No owned traffic channel (SEO, content, YouTube, community)

No recurring revenue mechanism

No diversified ad platform mix

Revenue tightly tied to ad performance

The model is performance-marketing optimized rather than brand-compound optimized.

There is significant upside potential in:

SEO expansion

Content marketing

YouTube vehicle-specific reviews

Influencer partnerships (automotive niche)

Retargeting email/SMS sequences

International scaling

The infrastructure exists to scale — but distribution remains concentrated and performance-dependent.

Marketing & Customer Acquisition

Goal: Is growth engineered or improvised?

Paid Ad Presence

All revenue is generated through Meta (Facebook) and Google Ads, indicating a performance-driven acquisition model. The presence of a dedicated creative director, video editor, and performance-based ad agency suggests structured paid media execution rather than casual ad boosting.

However, channel concentration is high. There is no evidence of TikTok Ads, YouTube Ads, affiliate marketing, or marketplace-driven acquisition. Growth currently depends almost entirely on two platforms.

Creative Sophistication Level

Moderate to strong.

The business employs:

A Creative Director (concept ideation and briefs)

A Video Editor (production execution)

UGC-style content (limited library)

This suggests structured creative testing. However:

Content library is limited

Specialty differentiation (integrated seatbelts, molded headrests, classic cars) has not yet been fully leveraged in ad storytelling

Heavy reliance on founder-shot content creates brand bottleneck risk

Creative sophistication is operationally organized but underdeveloped in narrative depth.

Funnel Depth

This is where the brand stands out.

Key differentiator: phone-based abandoned cart recovery.

Leads exported daily into GoHighLevel (GHL)

7% close rate

35–40% of monthly revenue attributed to this channel

This indicates:

Strong backend monetization

Structured CRM usage

Multi-touch sales approach

However, funnel depth outside phone calls appears limited. There is no mention of:

Lead magnets

Educational content funnels

Pre-purchase email nurturing sequences

Advanced retargeting segmentation

The funnel is conversion-focused rather than brand-building focused.

Email List Size

Disclosed email subscribers: 6,665

For ~13,000+ customers and ~157,000+ annual visitors, this list is moderate but underleveraged. There is no indication of strong email revenue contribution. Email currently appears to function more as a database than a revenue engine.

Organic Social Engagement

Public social accounts exist (Instagram, Facebook), but engagement levels appear modest relative to revenue scale.

There is no evidence of:

Strong community engagement

Consistent viral or high-engagement content

Educational long-form automotive content

Organic presence appears supportive rather than demand-driving.

UGC Density

Limited but present.

Given the high-ticket nature and strong product visuals, this category is well-suited for:

Before/after installs

Owner testimonial videos

Installation walkthroughs

Fit validation proof

Currently, UGC depth appears insufficient relative to the trust required for a $500 purchase.

Influencer Presence

No structured influencer program mentioned.

Automotive niche influencers (truck channels, restoration channels, detailing creators) represent an obvious but currently untapped acquisition layer.

CAC Indicators

Exact CAC is not disclosed.

However:

AOV: ~$430–$500

COGS: ~$160

Net margin: ~26%

Consistent $10k+ monthly profit

This implies CAC is currently sustainable but likely meaningful, given paid-only traffic and low CVR (0.6–0.7%).

The low CVR suggests acquisition efficiency could materially improve through conversion optimization and trust enhancement.

Scalability Signals

Strong scalability signals:

Proven paid acquisition engine

Structured creative team

CRM + phone sales backend

Outsourced ad agency scaling performance

Hands-off fulfillment

Major upside levers:

Increase CVR from 0.7% to 1%+

Add SEO

Expand content depth

Introduce non-leather materials

Diversify paid channels

Launch influencer partnerships

The model has growth levers, but they are not yet fully engineered.

LTV Indicators

Low natural repeat rate (seat covers are typically one-time purchases per vehicle).

However, LTV can be enhanced through:

Multi-vehicle ownership

Cross-sells (floor mats, interior packages)

New material launches

Upselling from partial to full custom

Currently, LTV appears primarily transaction-based rather than lifecycle-optimized.

Monetisation & Unit Economics (Surface-Level)

Goal: Does the math look structurally viable?

Pricing Strategy

The brand operates with a premium pricing strategy positioned around precision fit, leather material, and complex-seat compatibility. The offer is differentiated on quality and technical capability rather than price leadership.

Two pricing tiers exist:

Standard Custom Fit (partial back coverage, lower production complexity)

Full Custom Fit (360° wrap) (higher complexity, premium pricing)

This tiered structure supports value-based pricing and segmentation of budget-sensitive vs premium buyers.

AOV

Reported AOV: $430–$500

This is strong for an automotive accessory category and supports paid acquisition economics. High ticket size allows the business to absorb paid traffic costs and still maintain profitability.

Product Price Bands

While exact price bands are not disclosed, inferred range appears to be:

~$350–$600 depending on seat configuration and customization level

Given:

Average COGS ≈ $160

Reported net profit margin ≈ 26%

Consistent $10k/month profit

The pricing structure supports both paid acquisition and operational overhead.

Implied Gross Margin

Assuming:

AOV ≈ $430

COGS ≈ $160

Implied gross margin before ad spend ≈ 63%

After marketing and operational costs, net margin sits around 26%, which is healthy for a paid-traffic DTC model in a custom product category.

This indicates structurally viable unit economics, provided CAC remains stable.

Bundles/Upsell Logic

Current monetization structure appears relatively simple:

Front + rear seat configurations

Standard vs Full Custom

Some bundling exists but appears under-optimized.

Opportunities include:

Interior package bundles

Floor mats cross-sell

Installation accessories

Premium material upgrades

Express production upgrade

Upsell logic exists but is not fully maximized.

Return/Refund Signals

Refund rate reported at 0%, which is unusually strong for a custom product category.

This suggests:

Good expectation setting

Accurate VIN-based fit validation

Strong post-purchase support

However, lack of third-party review depth makes independent verification difficult. Still, operationally this is a positive signal.

Subscription Logic

There is no natural subscription model.

Seat covers are:

Non-consumable

Long lifecycle products

Vehicle-specific

Repeat purchase relies on:

Multi-vehicle ownership

Vehicle replacement

Upgrading to full custom

No built-in recurring revenue mechanism.

Margin Expansion Potential

Several levers exist:

Bulk production for top vehicle SKUs

Could reduce per-unit COGS significantly.Material diversification (non-leather)

Lower material cost SKUs for hot-climate markets.Conversion rate optimization (0.6–0.7% → 1%+)

Would dramatically increase contribution margin.SEO acquisition

Reduces blended CAC and improves net margin.Operational refinement of custom workflows

Standardization for top-selling vehicles.

Margin expansion appears feasible without changing pricing.

Brand Strength & Perception

Brand Consistency

The site, product positioning, and messaging are consistent around one core theme: “truly custom fit.” The VIN-based validation and complex-seat compatibility reinforce this positioning. Social channels exist but are modest in depth and engagement. Brand visuals are clean but not iconic.

Emotional Positioning

Primarily functional with confidence-based reassurance.

The purchase driver is accuracy, fit, and protection—not aspiration or status. There is some pride-of-ownership appeal (truck/classic car owners), but branding is not yet aspirational or lifestyle-led.

Storytelling Depth

Moderate but underdeveloped. The origin story (gap in poorly fitting covers) is clear. However, differentiation around integrated seatbelts, molded headrests, and classic cars has not been fully leveraged in long-form content or storytelling assets.

Founder Visibility

Founder-led narrative present. However, some marketing content relies on founder-created videos (not transferable), creating minor brand continuity risk post-sale.

Review & Trust Signals

0 Trustpilot reviews

Limited third-party validation

Refund rate reported at 0%

Trust infrastructure is weak relative to ticket size.

Community & Press

No meaningful press, certifications, or strong community layer visible.

Brand Defensibility

Operational differentiation (VIN validation + complex seat coverage) is the primary moat. No IP protection. Brand equity is emerging but not yet entrenched.

→ Brand Asset Strength: Moderate (Product-forward, not yet brand-driven)

→ Reputation Risk Flags: Lack of third-party reviews, limited social proof, founder-content dependency.

Competitive Landscape

Seat covers are a crowded category with many generic and mid-tier competitors. However, the true custom leather niche for complex seats is narrower.

Competitive Dynamics

Many universal-fit sellers

Few high-complexity fit specialists

Limited players handling vintage or integrated seatbelt seats

Pricing tiers range from $100–$600+. FCC sits at the premium end.

Switching Cost

Moderate psychological switching cost once VIN and measurements are submitted. Low physical switching cost pre-purchase.

Barriers to Entry

Low for generic sellers. Higher for:

Complex seat mapping

Supplier coordination

VIN validation workflows

Phone-based backend sales

Not race-to-the-bottom, but commoditization risk exists if others replicate systems.

→ Competitive Intensity Rating: Moderate-High

→ Positioning Gap Opportunities: Own the “fit guaranteed” authority position with education + comparison SEO.

Operational Complexity (Inferred)

SKU Complexity

High variability due to vehicle-specific customization.

Supply Chain

Custom factory in China; appears relationship-based. Likely single-supplier concentration risk.

Fulfillment

Made-to-order + 7-day shipping. Complex but systemized.

Returns

Reported 0% refund rate; operationally positive.

Cash Flow

No bulk inventory held (dropship model), reducing inventory burden but increasing per-unit COGS.

→ Operational Risk Score: Moderate

→ Scalability Friction Points: Supplier reliance, customization workflow complexity, phone sales dependence.

Risk & Fragility Signals

100% paid traffic dependency

35–40% revenue from phone recovery

No SEO engine

Low CVR (0.6–0.7%)

No structural IP moat

→ Fragility Index: High-Moderate

Top 3 Structural Risks:

Platform dependency (Meta/Google)

Supplier concentration

Weak trust infrastructure for high-ticket category

Growth Levers (Externally Visible)

SEO Domination for vehicle-specific and comparison keywords

Material Expansion (cloth options for hot climates)

Bulk production of top SKUs to improve margins

Influencer partnerships in truck/classic niches

Conversion rate optimization to 1%+

Founder & Operator Signals

This appears system-driven rather than hobby-driven.

Team in place: support rep, closer, creative director, editor, ad agency, fulfillment manager.

Owner claims 1 hour/day involvement.

Over-reliance on founder face in some creative, but not structurally dependent on founder for operations.

→ Operator Dependency Risk: Moderate-Low (systems exist, but creative identity partly founder-tied)

Exit & Optionality Signals

Strategic buyer appeal:

Automotive accessory roll-up

Performance marketing operators

Amazon aggregators expanding into DTC

Multiple expansion possible if:

SEO added

CVR improved

Margin increased

What improves with scale:

Supplier leverage

Brand authority

Content moat

What worsens:

Ad cost inflation exposure

→ Exit Attractiveness Score: Moderate-High

“Unfair Advantage” Check

Hard-to-copy elements:

VIN-based workflow

Complex seat mapping

Backend phone closing system

Supplier relationship

Replicable within 12 months by capable operator, but not instantly.

No IP, no community moat, no proprietary data moat yet.

Financial Snapshot (Preliminary Review)

Revenue: ~$550k

Profit: ~$134k annualized

Margin: 26% net

Multiple: 2.1x profit

Revenue appears consistent with Q4 spike.

Low refund rate supports stability.

Valuation is reasonable for a paid-traffic DTC asset.

Appears moderately optimized for sale (clear systems narrative).

Key Unknowns to Validate

Last 6 months revenue breakdown

True blended CAC & ROAS

Exact gross margin after shipping

Phone sales CAC vs ad CAC

Supplier contract security

Ad account health

Chargeback rate

Detailed reason for exit

Customer acquisition cost trend

Production bottleneck constraints

Preliminary Verdict

Opportunity Level: Moderate to High

Risk Level: Moderate-High (platform concentration risk)

Investment Profile:

Performance-driven cash-flow asset with brand build upside.

Best suited for:

Operator who can add SEO + brand authority

Buyer comfortable managing paid acquisition

Potential roll-up candidate in automotive niche

Not yet a deep brand moat — but structurally profitable with scalable upside.