Executive Snapshot

This is a high-velocity, high-margin supplement brand operating in a large and growing ingestible beauty category (Astaxanthin market $900M+), with strong early traction, a 45% repeat rate, and unusually favorable supplier financing terms (0% inventory funding). At <1.2x profit multiple, the listing appears materially undervalued relative to typical supplement exits (often 2.5x–4x+), suggesting potential pricing inefficiency or underlying risk not yet visible.

Initial Concern Flags

Heavy Meta ads dependency for acquisition (founder-managed media buying).

Regulatory exposure in supplement claims (skin tone / tanning positioning).

China-based manufacturing + concentration risk with a single supplier.

Extremely low multiple may indicate seasonality risk, performance volatility, or inflated recent profit.

Business is only 1 year old,with a limited durability track record.

Fast Signal Summary (Preliminary Read)

Conversion Rate: 4.46% (strong for supplements)

AOV: $85.80 (healthy for margin leverage)

Returning Customer Rate: 45% last 120 days (excellent signal)

Orders: ~28.7k

Sessions: ~598k

Peak Revenue Month: $572K

Subscription Launched: Sept 2025 ($30K MRR in first 30 days)

Immediate Internal Question

At $600K asking for $656K net profit, this is effectively a <1x profit acquisition.

This is either:

A distressed / risky asset masked by strong recent numbers

A highly seasonal spike business

Or an unusually strong asymmetric opportunity

The seller call must clarify which of these three it is.

2. Market & Demand Signals

The tanning supplement niche sits within the broader beauty-from-within and nutraceutical markets. While “tanning supplements” itself is a relatively small search term, it benefits from strong adjacent category growth. The global beauty supplement market is expanding steadily, and Astaxanthin (the brand’s core ingredient) is part of a fast-growing antioxidant segment with increasing consumer adoption.

Google Trends over the past five years shows cyclical spikes rather than structural decline, indicating seasonal interest (peaks before summer) with a stable baseline. This suggests demand is seasonally amplified but not collapsing. Search volume for broader skin health and antioxidant supplements remains significantly stronger than niche tanning keywords, which supports repositioning potential beyond seasonal tanning.

The problem is discretionary (appearance-driven rather than essential), but macro tailwinds are favorable: rising UV-awareness, growth in male grooming, wellness integration, and social media–driven beauty routines.

Regulatory exposure is moderate due to supplement claim compliance requirements, but the category is legally established in the U.S.

Market Attractiveness Score: Moderate–Strong

Demand Durability: Sustainable with seasonality; stronger long-term positioning if framed as skin health + wellness rather than purely tanning.

Product–Market Fit Indicators

Goal: Does this solve a clear problem for a defined audience?

Answer: Yes.

Value Proposition Clarity

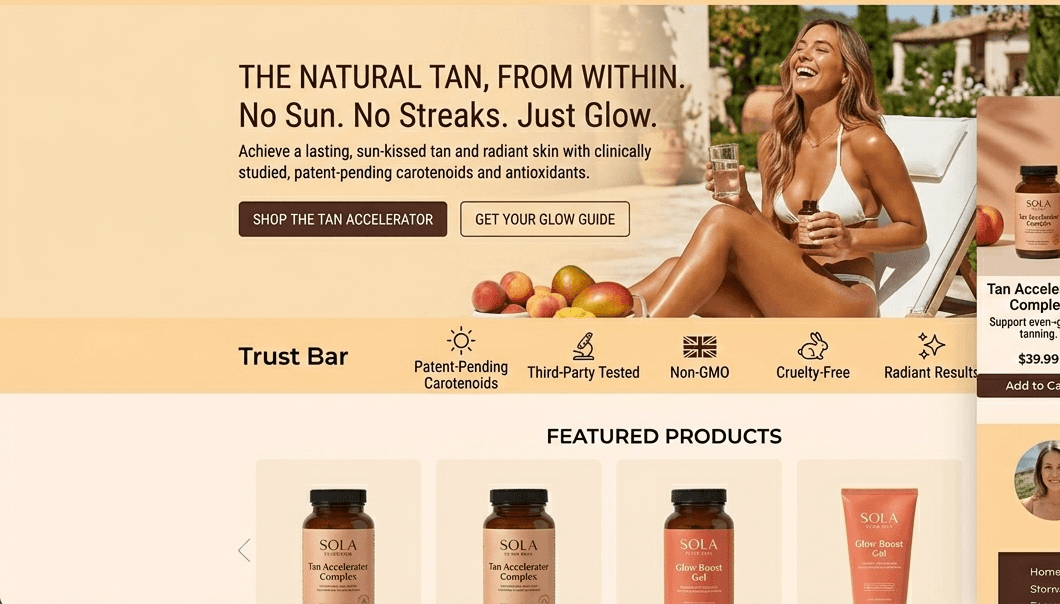

The brand offers a supplement designed to help men achieve a natural-looking tan year-round without UV exposure while supporting overall skin health.

Core Customer Persona

Health-conscious U.S. men focused on appearance, convenience, and wellness. Likely 20–40 years old, gym-oriented, image-aware, and active on social media. Motivated by aesthetics but prefers a “health-forward” solution over tanning beds or topical products.

Differentiation

Positioning is the strongest differentiator: male-focused ingestible tanning using Astaxanthin rather than topical self-tanners. Early-mover advantage within a niche male demographic. However, no visible proprietary IP or patented formulation. Brand-driven differentiation more than product defensibility.

Commoditisation Risk

Moderate–High. Astaxanthin is not exclusive and competitors can replicate formula and positioning. Brand equity and customer list are primary moats.

Ease of Adoption

Very easy. Capsule-based supplement with no behavior change beyond daily intake. Low friction purchase.

Repeat Usage Potential

Strong. Consumable format with visible aesthetic benefit supports recurring demand. 45% returning customer rate (last 120 days) reinforces this.

Subscription / Refill Logic

Subscription launched Sept 2025 and reached $30K MRR quickly. High compatibility with recurring model. Average order value ~$89 supports healthy LTV potential.

Price Positioning

Premium tier. AOV ~$85–$89 indicates strong perceived value, especially for a single-item order (1.0 item per order).

PMF Confidence Level: High

Differentiation Strength: Moderate (brand-led, not IP-led)

Website & Conversion Infrastructure (Updated – Reviews Included)

The Shopify store website is clean, modern, and aligned with wellness-focused men’s grooming brands. Mobile experience is intuitive, and the narrow catalog (single core SKU) reduces decision fatigue while keeping the purchase journey simple.

With an AOV of ~$89 and a ~4.46% conversion rate, performance is materially above standard ecommerce benchmarks, indicating the funnel is efficiently converting paid traffic. Checkout is streamlined, and subscription options are clearly integrated, minimizing friction.

Trust & Social Proof Signals

There are no Trustpilot reviews, which is a visible gap in independent third-party validation. However, the brand has 81 reviews on Amazon with an average rating of 3.6 stars.

A 3.6★ rating is mixed. It suggests the product works for many users but may generate inconsistent results or unmet expectations for others. In supplements ,particularly appearance-driven products ,perception gaps can directly impact retention and brand credibility.

Key implications:

Amazon provides external proof of real customers.

The rating is not strong enough to serve as a premium trust signal.

Mixed reviews may explain why the brand relies heavily on paid acquisition rather than organic reputation flywheel growth.

Overall Assessment

The conversion infrastructure is strong from a performance standpoint, but reputation infrastructure is underdeveloped. Strengthening review management, improving rating consistency, and adding third-party credibility badges could materially enhance long-term conversion stability and brand defensibility.

Traffic & Distribution Footprint

Goal: Where does demand actually come from?

The store generated approximately 598,000 sessions over the reported period, converting at 4.46%, indicating strong funnel efficiency relative to traffic volume.

Primary Channels

Acquisition is primarily paid traffic–driven, led by Meta (Facebook/Instagram) and Google Ads. Amazon provides an additional sales channel, while email/SMS supports retention and repeat purchases. Organic SEO presence appears secondary to paid acquisition.

Channel Concentration Risk

High reliance on Meta for top-of-funnel traffic creates concentration risk. Founder-managed media buying increases key-person dependency. If paid efficiency declines or ad accounts are disrupted, revenue could contract quickly.

Platform Dependency Risk

Meta dependency is significant. Google provides secondary stability. Amazon presence diversifies distribution but remains platform-controlled. TikTok and affiliate channels are not yet fully leveraged, representing both risk (current under-diversification) and opportunity.

International vs Local Reach

Customer base is primarily U.S.-focused. Limited visible international expansion suggests geographic concentration risk but also expansion upside.

SEO Footprint Strength

No evidence of strong organic authority. Traffic likely performance-driven rather than search-driven, reducing long-term defensibility.

Marketplace Presence

Amazon operates largely on autopilot, adding diversification. DTC remains the core revenue driver.

Direct vs Intermediary Sales

Majority appears direct (Shopify), with Amazon as supplementary.

Traffic Fragility Score: Moderate–High

Channel Diversification Strength: Moderate (paid-heavy with partial Amazon support; expansion channels underdeveloped)

6. Marketing & Customer Acquisition

Goal: Is growth engineered or improvised?

Growth appears engineered, performance-driven, and creatively structured, but highly dependent on paid acquisition.

Paid Ad Presence

Meta (Facebook/Instagram) is the primary acquisition engine, managed directly by the owner. Google Ads supports bottom-of-funnel intent capture. Amazon operates as a secondary channel with established campaigns. There is no meaningful TikTok Shop or affiliate engine yet, indicating unrealized diversification.

The brand surpassed $1M within six months and reached a $572K peak month ,strong evidence of paid media effectiveness and scalable ad execution.

Creative Sophistication

The in-house creative team (2 video editors + 1 strategist) produces weekly ad variations, suggesting structured creative testing and iteration. This is not improvised marketing; it is systematic performance marketing. Internal creative control reduces agency drag and supports faster scaling.

Funnel Depth

Funnel structure includes:

Paid traffic (Meta top-of-funnel)

Google search retargeting / branded capture

Email & SMS retention flows

Subscription offer (launched Sept 2025)

A Head of Funnel oversees CRO, post-purchase upsells, and lifecycle email ,indicating layered funnel optimization rather than single-step selling.

Email List

36,403 subscribers from 37,415 customers indicates strong capture mechanics and list penetration. This is a valuable asset.

Organic & UGC

Organic presence appears secondary to paid. There is no major visible influencer ecosystem yet. UGC likely exists within paid creatives, but brand-level organic authority seems limited.

CAC & Efficiency Signals

While CAC is not explicitly provided, 25% net margins at scale in a supplement business imply controlled acquisition costs. Peak season (Jan–June) focuses on aggressive acquisition; off-season shifts to retention, improving profitability due to lower ad spend and ~40–45% returning customers.

The P&L structure (25% net margin) suggests media spend is heavy but sustainable under current performance.

LTV Indicators

45% returning customers (last 120 days)

Subscription launched → $30K MRR within 30 days

$85–$89 AOV

Consumable product

These are strong early LTV signals, particularly for a 1-year-old brand.

Scalability Signals

Positive:

Inventory financing at 0% interest reduces working capital friction.

Lean in-house team already structured.

Proven ability to scale paid ads to $500K+ months.

Constraints:

Founder dependency for Meta scaling.

High platform concentration (Meta).

Limited channel diversification.

Output

Marketing Maturity Level: High (performance-structured, team-driven, not ad-hoc).

Scalability Assessment: Strong but platform-dependent. Scales efficiently within paid ecosystems; long-term durability requires channel diversification (TikTok, affiliates, SEO, influencer networks).

Monetisation & Unit Economics (Surface-Level)

Goal: Does the math look structurally viable?

Pricing Strategy

Premium positioning for a single-SKU ingestible supplement. Price signals confidence rather than discount-driven acquisition.

AOV & Price Bands

AOV sits around $85–$89 with 1.0 items per order, indicating the product itself carries high ticket value rather than relying on bundles.

Implied Gross Margin

With ~25% net margin after paid ads, team, and overhead, gross margin is likely strong (typical supplement gross margins 65–80%). Inventory financing further enhances effective margin efficiency.

Bundles / Upsell Logic

Limited visible bundling. Opportunity exists to introduce multi-bottle packs, auto-ship discounts, or complementary SKUs to increase basket size.

Return / Refund Signals

Refund rate reported at 0.0% with 99.2% fulfilment rate. If accurate, operational leakage is extremely low. Needs verification.

Subscription Logic

Subscription was recently launched and already meaningful. Strong early adoption indicates recurring revenue potential.

Margin Expansion Potential

Lower CAC in off-peak months

Bundle introduction

Subscription penetration growth

International pricing arbitrage

Economic Health Estimate: Strong for a 1-year-old brand.

Monetisation Sophistation: Moderate–High (room for expansion via bundling and product line depth).

Brand Strength & Perception (Updated – Review Context Included)

Goal: Brand asset or product storefront?

The ecommerce store presents a consistent brand identity across its website and positioning: male-focused, health-forward, and positioned around aesthetic enhancement through supplementation rather than cosmetic vanity. The messaging blends wellness and appearance, which is strategically aligned with current beauty-from-within trends.

Emotional positioning leans toward aspirational confidence and convenience, not luxury or status. The angle is clear and differentiated, but the broader brand narrative ecosystem (community, transformation stories, brand mission depth) remains underdeveloped.

Founder visibility appears operational rather than consumer-facing. The brand does not currently leverage personality-driven authority as part of its perception moat.

Review & Social Proof Signals

There are no Trustpilot reviews, which limits third-party credibility in the DTC environment. However, the Amazon listing shows 81 reviews with an average rating of 3.6 stars.

A 3.6★ rating is mixed ,not alarming, but not strong enough to function as premium validation. This suggests:

The product resonates with a portion of customers.

There may be variability in results or expectation alignment.

Reputation strength is still forming.

There are no visible major press features, certifications, or partnerships adding authority.

Community presence appears limited; the brand has not yet evolved into a lifestyle movement with strong organic advocacy.

Brand Asset Strength: Moderate

Reputation Risk Flags: Mixed Amazon rating (3.6★) and absence of independent third-party review authority.

Competitive Landscape

The supplement space is crowded; ingestible tanning is niche but replicable. Larger supplement brands with stronger distribution could enter.

Pricing sits in the premium-mid tier. No race-to-the-bottom pricing currently.

Switching costs are low; customers can try alternative supplements easily.

Barriers to entry are moderate: formulation is accessible; brand execution is the differentiator.

Competitive Intensity Rating: Moderate–High.

Positioning Gap: Male-first aesthetic supplement positioning remains relatively underdeveloped.

Operational Complexity (Inferred)

Single core SKU simplifies operations.

However, reliance on one overseas manufacturer introduces supplier concentration risk.

Supplement compliance creates regulatory exposure (claims, labeling).

Low refund rate reduces customer service burden.

Inventory financing reduces working capital strain, lowering cash-flow sensitivity.

International expansion would introduce complexity (regulatory + shipping).

Operational Risk Score: Moderate.

Scalability Friction Points: Supplier dependency; regulatory oversight.

Risk & Fragility Signals

Hero SKU dependency is high. Paid channel reliance increases fragility. Platform policy exposure exists (Meta, Amazon). The product is partially trend-driven. Product moat weaker than brand moat. Replication is straightforward.

Fragility Index: Moderate–High.

Top 3 Structural Risks:

Paid media disruption

Supplier concentration

Regulatory/claim compliance

Growth Levers (Externally Visible)

Adjacent supplements (skin health, antioxidants, male grooming stack)

Geographic expansion beyond the U.S.

Retail or specialty fitness distribution

Subscription penetration scaling

Influencer + TikTok Shop rollout

Actionable Hypotheses:

Launch 2–3 complementary SKUs within 12 months

Push subscription penetration >30%

Build influencer affiliate engine

Expand into EU/AUS markets

Develop bundle strategy to raise AOV to $110+

Founder & Operator Signals

The founder is a performance marketer. Growth execution appears structured, not accidental.

Clear team roles and SOPs exist.

However, Meta ads remain founder-managed ,key-person risk.

Business feels professionally run, not hobbyist.

Operator Dependency Risk: Moderate (ads scaling tied to founder expertise).

Exit & Optionality Signals

At <1x profit multiple, this is unusually discounted versus supplement industry norms.

Appeals to:

Supplement roll-ups

PE micro-aggregators

DTC operators

Multiple expansion potential exists if:

Revenue stabilizes across seasons

Channel diversification improves

SKU expansion reduces fragility

Exit Attractiveness Score: High (pricing inefficiency creates asymmetry).

“Unfair Advantage” Check

Hard-to-copy asset: Early brand traction + email list + paid creative engine.

No IP moat.

Data moat (37K+ customers) is meaningful.

Inventory financing advantage is unique but may depend on relationships.

What’s hardest to replicate quickly: existing paid ad learning + customer list.

Financial Snapshot (Preliminary)

Revenue grew rapidly; peak months indicate scalability.

Margins stable around 23–25%.

Multiple extremely low vs industry (2.5x–4x typical).

Numbers appear optimized but not obviously inflated.

Needs monthly breakdown verification for seasonality depth.

Key Unknowns for Seller Call

Last 6 months monthly revenue breakdown

True gross margin %

Blended CAC & ROAS

Verified LTV

Confirmed refund rate

Supplier contract terms (exclusivity?)

Inventory on hand

Reason for selling

Owner post-sale involvement

Largest operational bottleneck

Preliminary Verdict

Opportunity Level: Asymmetric

Risk Level: Moderate–High

Investment Profile:

Arbitrage opportunity + brand build play + potential roll-up candidate.

At sub-1x profit multiple, upside outweighs visible risk ,conditional on validating seasonality stability and paid channel resilience.